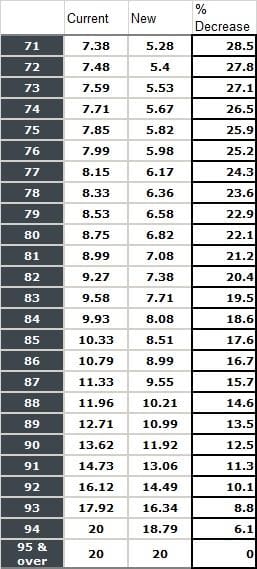

Many Canadian seniors will be surprised when their RRIF payments decline by as much as 28% in 2016. Seniors age 82-and-under will see a decrease of at least 20%*

Seniors that chose to receive the RRIF minimum payment will be most affected. That minimum is determined by the market value of your plan assets as of the previous December 31st, multiplied by the CRA age factor. But in the 2015 Federal budget, the RRIF minimum factor was significantly reduced (see table below). And if your amount withdrawn exceeded your plan growth in 2015, your pay cut will be even deeper.

You’re a senior and your financial advisor has not spoken with you about this? Here are a few suggestions:

Up to now, if the minimum has been more than you needed, you might have manually or or automatically moved the excess to a TFSA or other account. Consider adjusting that amount downward, or outright cancelling it when your RRIF payments decline next year.

If the minimum has been less than you needed, you may have been withdrawing additional funds from a TFSA or non-reigstered account. If those withdrawals were automated, you may want to increase the withdrawal amount to offset your reduction in RRIF income.

You may have a one-time opportunity to re-deposit an excess amount to your RRIF to reduce your 2015 tax burden. The deadline is February 29, 2016.

Today’s longer lifespans are the reason for the change in the RRIF tables. The federal government’s concern (the concern of every senior and their advisor) is that the existing formula forced seniors to deplete their RRIFs too aggressively, and risk running out of money prematurely.

Let’s say you’re a Canadian senior. Now is a particularly good time to re-assess whether your portfolio withdrawals (irrespective of the changing RRIF rules) are sustainable, keeping in mind ever-increasing life expectancy. And don’t be shy about reaching out on this tricky issue – it’s mission-critical!

*The above table is based on CRA data found here.

Rona Birenbaum is a certified Financial Planner and is licensed to do financial planning. Rona is registered through separate organizations for each purpose and as such, you may be dealing with more than one entity depending on the products purchased. Rona is registered through Caring for Clients for financial planning services. This website is not meant as a solicitation for financial advisory services. Financial advisory services are available through the facilities of Monarch Wealth Corporation. Financial Planning is not the business of or under the supervision of Monarch Wealth Corporation and Monarch Wealth Corporation will not be liable or responsible for such activities.